The Housing Market is in Trouble

Follow our Instagram page and Linkedin Page !

Sign up for our email list to receive each article in your inbox!

Hi all, this week we have seen troubling data released on US housing, and we take a look at the message that has come from the Jackson hole central banker’s symposium. There has also been major developments on how Japan intends to source its energy, and one car manufacturer has not held back in its attempt to cut costs. Enjoy!

Building Bust en route?

Data released by the US Census Bureau and US Department of housing this month showed that the number of new private home buildings starts decreased MoM from June to July by 9.6%, the biggest dip since the beginning of the Covid pandemic. This has been driven by rising mortgage rates as a result of the various rate hikes implemented by the Fed over the last few months, as well as high building costs as a result of inflation. The housing market is a great indicator of the overall direction that an economy is headed, so this data will not help the bulls case that the market lows are in.

In a ‘hole’ lotta trouble

This week’s Jackson hole event in Wyoming gave Federal Reserve Chair Jermone Powell the stage to deliver a very hawkish message, warning that interest rates will have to stay at a level that restrains growth “for some time” if inflation is to be tamed. This caused major markets such as the S&P 500 and the NASDAQ 100 to tumble on Friday, as investor confidence was rattled by Powell’s words. In the last few weeks markets had climbed based on expectations of easing interest rate hikes from the Fed off the back of a fall in US inflation for July, but Jackson Hole 2022 has clearly shown that this isn’t the case.

New-Clear Energy

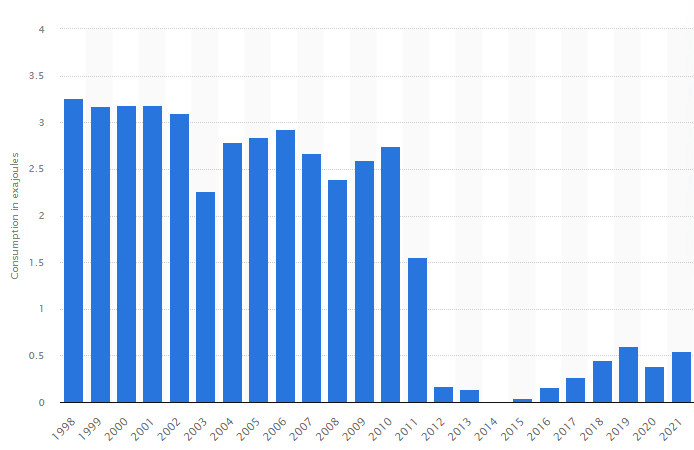

This week the Japanese Prime Minister, Fumio Kishida, announced he has appointed an internal government team to investigate the use of newer and safer nuclear reactors in order to help Japan toward its goal of Carbon Neutrality by 2050. This is a major change in policy after Japan’s decision to phase out its dependence on nuclear energy after the Fukushima disaster of 2011. Kishida also recognised that the government would need to win over the public as they turned against nuclear energy after the disaster, though government officials believe voters may now be more open to nuclear given the steep rise in energy prices, as well as climate change factors. The appointed team is to report back with their ideas by the end of 2022. One holding in The Spark’s Portfolio, Cameco, rose 16% on the news.

Nuclear energy consumption in Japan 1998-2021, Source: Statista

Ford sharpens its Axe

Ford Motor this week announced its intentions to sack 3,000 employees in an effort to reshape its labour force as it plans to invest tens of billions into the production of electric vehicles (EV). Ford executives described the company’s cost structure as “uncompetitive” compared to other manufacturers in the EV market. This follows the split of the car maker into two separate businesses in March, one for combustion engine vehicles and one for EVs. In Europe, where there have also been large staff cuts, Ford has committed to making all of its passenger cars electric by 2030. The tight labour market may not remain that way for much longer…

Oily Affairs

This week Saudi Arabia announced that it could cut oil production, as Biden plans to revive a nuclear energy deal alongside a return of oil production with Saudi rival, Iran. Oil prices, which have slid $25 a barrel since June, quickly jumped back up to over $100 dollars a barrel after the Saudi announcement was made. The move from Saudi Prince Abdelaziz Bin Salman has been seen as a way of warning the US of the consequence of facilitating the return of Iranian oil to the Global markets, which would drive down oil prices if there were no other production cuts. State-owned Saudi Aramco made record profits in Q2 of $48bn, and the Prince doesn’t want this to end anytime soon.

Hope you enjoyed this week’s Market Wrap!

Patrick

Disclaimer

This communication is for informational and educational purposes only and should not be taken nor used as investment advice, as a personal recommendation, or solicitation to buy or sell any financial instrument. This material has been prepared without considering any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or structured product are not, and should not be taken as, a reliable indicator of future performance. I assume no liability as to the accuracy or completeness of the content of this publication.