Flash Note: Are We Entering a Bear Market?

Recent developments regarding rising Ukraine-Russia tensions are worrying me, so I feel it is prudent to release a short note, explaining my reasoning to sell Polymetal now. The US and UK are pulling diplomats from Ukrainian embassies as a result of growing tensions with Russia. Polymetal International is a Russian miner and therefore sanctions by the US and other nations will hurt their trade. In retrospect, I should have acted sooner on the developing tensions, but I believed the threat of invasion by Russia was a power-play by Putin to speed up the Nordstream 2 development. Once the risk-off market sentiment has waned, I will add another gold miner to replace POLY, for the reasons outlined below.

Alongside the sale of POLY, I am also selling my position in Pennon Group (PNN). With yields rising, alongside higher inflation, utilities will suffer as they struggle to pass costs to customers. PNN was a strong holding as yields fell because utilities provide safety in times of worry. However, it will now suffer as bonds sell-off (see below). I am disappointed with the sales of POLY and PNN. I underestimated the geopolitical risks for POLY. With respect to Pennon, I didn’t see the hawkish shift of the Federal Reserve early enough. Thankfully due to my position sizing the sale of both holdings will not result in a large loss, and they have not affected performance hugely. With the capital from the sale of PNN, I am rotating capital into Lockheed Martin (LMT), again once the dust settles. This is a lesson learned and something I will not repeat in the future.

PNN and long-bonds move in tandem, Source: TradingView

Bond-Equity Crisis Alpha

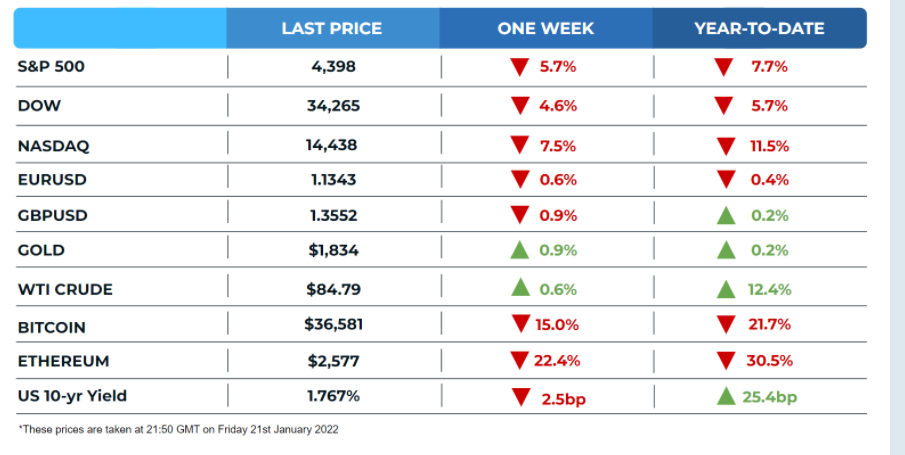

Bonds have traditionally provided investors a low correlation to equities, hence why many financial advisors recommend holding a portfolio with both bonds and equities. However, at times there is a higher correlation between the two – with bonds and equities (stocks) selling off in tandem. I was worried that this would occur, hence why I have avoided bonds and highly valued stocks (which would fall most). In the last few weeks, this has occurred, affecting the traditional 60/40 portfolios hugely (60% bonds 40% stocks). During the sell-off, the only safe haven was once again gold. Its presence in The Spark’s portfolio has been invaluable, as you can see below.

Gold holds up while everything else sells off

The Spark’s portfolio was up 8.8% from inception and 2.4% for 2022 prior to the market’s recent correction. It is now up 4.4% and -1.42% for 2022. This is compared to the S&P500 -8.3% return for 2022, and the NASDAQ’s -12.5% return. I am very happy with both this return and the drawdown of just 4.4% for my portfolio. Lower drawdowns are great because this shows the portfolio has a low correlation with the overall market. The outperformance is partly due to my avoidance of growth stocks, and partly due to my exposure to precious metals, both of which are helping me outperform the index’ and avoid a large part of the recent selloff (so far anyway).

In August 2007 and November 2020, there were huge ‘factor reversals’. This could happen again now. This occurs when institutional investors (and quants) unwind positions in growth and move to value stocks, causing one to tank while the other soars. This makes me lean toward adding further to my value holdings through financials or materials companies (not currently held in the portfolio). One worry that I have written about on several occasions is whether growth will sell off in isolation (i.e. rotation outlined above) or cause a market-wide selloff. I have continued to read white papers over the last week, and from this research, I have found that when volatility (measured by the VIX Index) is above 30, commodities begin to sell off in a big way. I had planned to add a materials stock to the portfolio, to gain exposure to the rotation outlined above. However, for now, I think it is sensible to sit on my hands. The recent sell-off started with tech, but I believe the capitulation is now spreading. This happens when funds are forced to sell other positions to cover margin calls and losses. After highly valued companies, commodities and others will now follow.

Volatility (VIX) vs Price performance for every asset class

The final action I am taking is to half my position in Airtel Africa (AAF). I have now made a 50% profit in just three months, and as you can see above, emerging market equities will suffer as the VIX continues to rise. In addition, the rising US Dollar and tightening liquidity market may lead to an outflow of capital from such markets. On a technical basis, RSI divergence has occurred, and the stock is due a correction, having risen so far in such a short period. I added Airtel as one of my largest positions and I still have huge conviction in the stock, but with 6.7% of capital now in the stock, any fall could hurt performance for the portfolio, so rebalancing at this price makes sense. However, I will not hesitate to add back to the position should it make a substantial fall.

The Federal Reserve meeting this week is of huge significance. If they ignore the recent sell-off and continue with their plans for interest rate rises and tapering, sit tight, as there will be a lot more downside to follow. There are a lot of weak retail hands, and this is the first significant downturn they have seen. The panic selling has only started if the Fed remains hawkish on Wednesday. If they assure markets, we could see a bounce. I will decide based on the market’s movements (and Fed’s comments) by the end of the week whether this is a time to buy the dip or a short the rip environment. With high inflation here, I feel the latter may be of greater likelihood.

With that being said, I just want to remind you all to relax. This may be the start of a bear market, or it may not be. Either way, this too shall pass. Don’t stress. If you have listened to my advice over the past few months by avoiding highly valued companies (and focusing on strong cash flow generative businesses) and holding a high level of cash, you will currently be in a great position. If you can’t stomach the downside you shouldn’t invest. Knowing what you own is critical when you see your investments down over 20% in a week (BioNTech, for example). For now, I wait with 29% cash on the side-lines and will unleash it when I see a bottom.

Action:

· Selling 100% of Pennon Group (LN: PNN) at £10.65 at a 9% loss (£28)

· Selling 50% of position in Airtel Africa (LN: AAF) at 150p, at a 50% gain (£115).

· Selling 100% of Polymetal International (LN: POLY) at £11.34 at a 15% loss (£47).

Portfolio Return Year-To-Date: -1.4% . Return Since Inception: 4.4%. Alpha above S&P500: 7.6%

Disclaimer

This communication is for informational and educational purposes only and should not be taken nor used as investment advice, as a personal recommendation, or solicitation to buy or sell any financial instrument. This material has been prepared without considering any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or structured product are not, and should not be taken as, a reliable indicator of future performance. I assume no liability as to the accuracy or completeness of the content of this publication.