Ten Potential Ten-Baggers

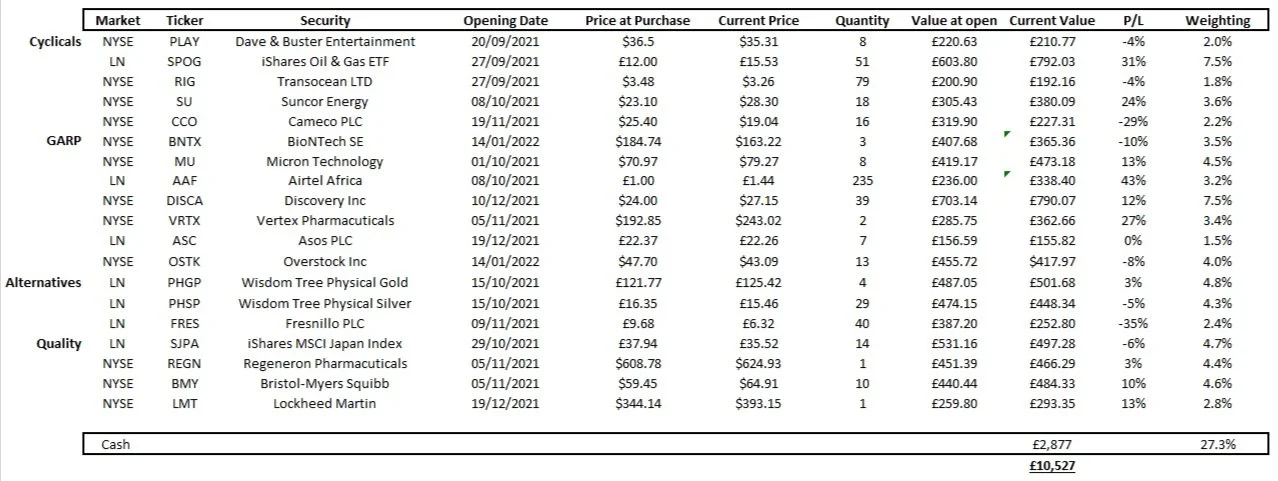

This week has been interesting. Federal Reserve (Fed) Chair Jerome Powell has confirmed the Fed’s actions to raise interest rates in March and for the commencement of quantitative tightening (QT) alongside or following this. Markets are pricing in four to five rate hikes this year. Powell did not rule out hiking at every meeting, so markets sold off. Inflation keeps rising; however, the rate of this increase is slowing. The inflation numbers over the coming months will be interesting, as supply-chain disruptions seem to be easing, so if the inflation figures start to fall it will be favourable for growth stocks once again. Retail sales are strong, but consumer confidence is low. I assume this is because the population is viewing rising costs (via inflation) as an uncertainty. There is significant weakness in the markets, with risk-off sentiment still present. The market is aggressively pricing in rate hikes and QT. I feel there may be some more downside weakness, especially for growth stocks, but we could be getting closer to a capitulation low. Should this stabilise over the coming weeks I will not hesitate to add growth stocks at depressed valuations. Corrections, even as deep as the one currently experienced, are healthy for rebalancing margin and removing weak hands from the market. Nothing is free in life. Volatility is the price you pay for stock market returns. Once I believe a market low is in place, I will post a flash note similar to the note posted earlier this week, loading up on the best opportunities that I find. For now, I think it is prudent to add a small amount to some existing positions, considering the 29% I currently hold as cash in the Spark portfolio.

Action:

Buying 1% of Overstock (OSTK) at $43.09

Buying 1% of BioNTech SE (BNTX) at $162.22

Let me be clear from the outset, none of these are current recommendations, and the prices I give are suggestions based on quick, back-of-the-hand calculations. I will only write about a company I would own myself, and in my opinion, has excellent prospects. However, I do not suggest buying several of the companies highlighted below at current valuations.

The FAANGs

I can’t start an article on tech without mentioning at least some of the FAANGs (Facebook, Amazon, Apple, Netflix, Google). These companies have grown to dominate every aspect of our lives, and some may continue to do so for a long time.

Amazon (AMZN) has benefitted hugely from the pandemic and many of us rely on its services regularly. It is pushing to achieve same-day delivery and have a number of subscription services that give it more assured revenue – such as Audible or delivery for a year. It is involved in AI, Space, Retail, groceries, and everything in between. AMZN truly has its finger in every pie. One segment of its business, Amazon Web Services (AWS), delivers cloud services. This is a high margin and fast-growing division, so will help to create margin expansion for the business. Amazon has traditionally been a lower margin tech name (around 5%), but AWS should help it change that. As a result, the market may apply an even higher multiple to its share price. The company is currently spending $50bn per year on capital expenditure (Capex), which will also help to contribute to sustained growth for many years to come. An attractive opportunity at current prices.

Meta (FB) is the next one I am monitoring. It owns Facebook, Instagram, Oculus, and Whatsapp, among others. Its sources of revenue are mainly from selling data and advertising. With the platforms it owns, its total addressable market (TAM) is monumental. This means its influence and ability to cross-sell products are massive. Also, FBs movement to the metaverse is testament to Zuckerberg’s ability to continue to innovate. Meta is acting like a start-up company with a cash pile a Saudi prince would be jealous of. Like Amazon, Meta continues to increase capex, expecting to spend around $30bn per year from 2022-2025. This comes alongside growing free cash flow, from $35bn for 2021, to an expected $63bn by 2025. If FB can become the forefront of innovation within the metaverse, much it has become with social media, the sky is the limit for its shares. At today’s prices, I am tempted.

Third is Apple (APPL). Much like those mentioned above, Apple’s brand awareness is huge and the demand for its products is very sticky. Once you buy one device, especially the iPhone, you tend to continue purchasing it. I can’t name one family I know without at least one Apple device, and most have multiple devices (mine included). The company dominates the mobile phone space but seems to be maturing more than AMZN or FB. This is difficult to value due to the huge intellectual property behind the brand, and the ever-increasing multiple the market is prepared to pay, so I will leave you to be the judge on this one.

Apple Inc (AAPL) EV/EBITDA multiple, Source: TIKR

PayPal (PYPL)

I don’t think the next name needs any introduction either. PayPal is one of the largest fintech and payment companies in the world. Its expansion into crypto has been an astute move by management and it currently has 416 million active users with a total payment volume (TPV) of over $300bn. Again, PYPLs ability to cross-sell is huge, and the company has a strong demand for its product given it was one of the first in the Fintech space. The business’ huge free cash flow will allow it to continue to innovate further into crypto and other ventures. I may add this to the portfolio in the coming weeks.

Thinksmart (TSL)

Sticking with the online payments niche, one small-cap stock set to benefit is Thinksmart (TSL). This company has equity stakes in a number of businesses, including a 10% call option on Afterpay (APT) – see bottom of link or bottom of article for explanation. APT (Clearpay in the UK) is a Buy Now Pay Later (BNPL) business for online shopping, which was recently acquired by Block Inc (SQ). Its revenue is growing at a cyclically adjusted growth rate (CAGR) of 81% and it is expected to become profitable this year. The 10% call option allows TSL to purchase a stake in the Afterpay anytime until 2023. This is likely to be bought over by Block Inc at a significant premium to TSL’s carrying value (the value it has marked for the call option in its books). The recent tech rout has seen TSL, Block, and Afterpay’s share price fall substantially, but this could be a great opportunity in advance of a potential buyout. The news of Afterpays takeover sent TSLs shares rockets 75%. A buyout could send it soaring higher once again, and that is without mentioning the companies other investments. This company is too small to be added to the Spark’s portfolio but looks like a great opportunity at current prices.

Stoneco (STNE)

Much like Airtel Africa (AAF), a holding in The Spark’s portfolio, another attractive emerging market fintech solutions business is STNE. This company provides digital payments and business solutions for retailers across Latin America and is currently growing revenues at 40% Year over Year. It has high operating margins of around 60% and continues to expand into new regions. Warren Buffet’s Berkshire Hathaway was an early investor, and the price has fallen over 80% in the last year. For the growth the business is currently experiencing, it is currently at an extremely attractive valuation. However, one major consideration is the exchange rate risks associated with this business. The countries it operates in experience major inflation risks, Brazil being one example, and others are adept at defaulting on debt (Argentina). The political risk involved in many of these countries is also a consideration. Much like the growth seen in Africa, Latin America’s smartphone affordability and internet reach continue to widen. This company has huge potential to capture this growth. However, I view STNE as a high-risk buy at current prices, so intelligent position sizing is very important.

Darktrace (DARK)

One successful tech company closer to home is Darktrace, a business which recently IPO’d on the London Stock Exchange. DARK is a tech business providing Artificial Intelligence (AI) cybersecurity for corporate customers worldwide. It has a well-diversified revenue by geography and a huge addressable market (see below). The COVID-19 pandemic has greatly increased the drive for technology advancement, as many companies move to hybrid working models and online businesses. Cybersecurity will be essential for this transition. DARK has a subscription model with average contract lengths of three years, giving the business assured, high-margin revenue streams. Darktrace’s technology self-learns to read the current operating systems of the corporate client. It then sets up niche firewalls depending on the companies specific situation, identifies weak points, and takes proactive action to prevent and guard against cyber-attacks. Because of this tailored service, recurring revenue is high, and customer churn is low. In addition, with companies like Vodafone and Tottenham Hotspurs as customers, its products are clearly top of the range. It has several product offerings available to clients, and over recent quarters has been able to significantly grow the number of products sold to each client. The company seems overvalued at present, but if it can continue to grow free cash flow it may be an interesting opportunity in the future. A speculative buy today in my view.

Darktrace TAM and Revenue by geography, Source: Darktrace.com

Advanced Micro Devices (AMD)

AMD is a semiconductor company producing graphics cards, high-performance gaming computers, and monitors. It is a high-quality business led by a strong management team. It has grown from negative free cash flow in 2018 to an expected $3.4bn for 2021. The boom in semiconductors looks set to continue into the end of the decade, and supply chain disruptions within this sector may be at play for another year or more, due to the extensive time and cost of building and calibrating new foundries. This will benefit AMDs pricing power as it is expected to continue to grow margins into 2025. At 24x EV/EBITDA the company is definitely attractive at current prices, and another company I may add soon to the Spark portfolio.

Overstock (OSTK)

I already own OSTK within The Spark’s portfolio, and I have written about it previously, but I believe this is one worth repeating. OSTK is one of the best opportunities I have seen in quite some time. It has a legacy furniture business which is an asset-light model, dropshipping all its products to customers. This side of the business has benefitted hugely from lockdowns, being exclusively online-based. The company is priced at 9x EV/EBITDA, a very fair multiple for a furniture business growing revenue at around 10% per year. On top of this, investors get a free equity stake in a venture capital business (Medici Ventures) and a crypto exchange (tZero). One of Medici’s company’s, Bitt Global, has recently announced a deal with the Nigerian government to release a Central Bank Digital Currency (CBDC). The businesses held in this portfolio could be worth millions, if not billions, and these are in the price for free. A strong buy at $43.

Agronomics (ANIC)

The final area of technology that seems interesting for a long-term bet is the future of food. Agronomics is a venture capital (invests in small start-ups) trust, investing in companies that are trying to create cultivated meat. This involves growing meat from animal cells in a lab. Over recent years, the cost of producing such meat has fallen substantially, and with the huge amount of resources and land used by animals, cultivated meat may be the future as we transform into a more sustainable world. It is a highly speculative buy that could pay off in the long term.

I hope this week’s article provided you with some ideas for further research. The market has dropped substantially over the last few weeks, and although I believe there is more downside still to come, it seems that we are nearing a bottom. That means it is time to go hunting for bargains.

“The man who can do the average thing when all those around him are going crazy”

I believe I have positioned the Spark’s portfolio well for this correction; with the large cash pile I have held recently. That was the average thing to do while everyone continued to rush into the market. It may be time to go hunting.

What is a call option?

A call option is the right but not obligation to purchase the shares of a company at a specified price on or before a specified time. A ‘call’ option is the right to buy, and a ‘put’ option is the right to sell (short) a stock. The buyer purchases this option paying a premium (a lump sum). The purchase of an option is essentially a leveraged bet on the company’s shares rising (call option) or falling (put option). If Investor A holds a call option for company B at a price of $10 per share, and pays a $1 premium, then their breakeven price for the option is $11. If the shares surge to $20, Investor A can exercise the call option and sell the shares, booking a $9 profit. However, if Company B’s share price falls to $2, Investor A can decide not to exercise the option (doesn’t buy the shares) and therefore the option contract expires worthless and they lose their $1 premium they paid to hold the option.

Portfolio Return Year to date: -0.65%

S&P500 Return YTD: -7.6%

Until next time,

Peter

Disclaimer

This communication is for informational and educational purposes only and should not be taken nor used as investment advice, as a personal recommendation, or solicitation to buy or sell any financial instrument. This material has been prepared without considering any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or structured product are not, and should not be taken as, a reliable indicator of future performance. I assume no liability as to the accuracy or completeness of the content of this publication.