The Magic Formula for Stock Picking

Click here to sign up for our weekly articles to be sent to your email inbox!

Over the last few months, I have listened to and read many investment-related books, one of which was ‘The little book that beats the market’ by renowned investor Joel Greenblatt. I would highly recommend the book as he simplifies all things related to investing and the stock market. The main aspect covered in the book however is his simple stock screener which has proven to outperform the market over the long term. His screen ranks every stock in the New York Stock Exchange (NYSE) based on its Return on Capital Employed (ROCE) and its Earnings Yield (Earnings per share divided by Share Price - the inverse of the PE Ratio). Then the screen adds these two ranks together. The lowest combined figure is the best company based on both valuation (earnings yield) and business efficiency (ROA/ROCE). This is the magic formula.

I have decided to put the book into practice, using the common sense of this investment approach and adding the skills I have developed in stock selection to choose several new stocks to add to the portfolio.

I used Greenblatt’s screen, which you can use for free here, to uncover undervalued but high-quality companies. After running the screen over the past few weeks, it was interesting to find that, using a minimum Market Cap of $10bn, two current holdings - Lockheed Martin and Regeneron - were both highlighted by the ‘magic formula’.

Companies that caught my eye included HP, Buckle, and Best Buy Co. These may be good companies for you to research further. The best opportunities, in my opinion, were found in GoPro Inc (GPRO), Crocs Inc (CROX), Meta Platforms (FB), and PayPal (PYPL), all of which have shown up on the screen in the last two weeks. Alongside these companies, I have found an exciting opportunity in Digital Turbine (APPS).

With the exception of Digital Turbine, I would assume readers know the core function of the businesses that I have outlined above. In the interest of brevity, I will outline my main thesis for each investment, and the reasons they are attractive today. I will cover GoPro, Crocs, and PayPal this week, with Meta (Facebook) and Digital Turbine being covered in two weeks’ time.

As I have mentioned recently, I feel that this is not the bottom for tech, however, these companies are at their lowest valuations in many years and are now at a price I believe is very attractive. Therefore, I am unphased by the macroenvironment when I know the long-term opportunity for each of these companies now outweighs the short-term price action, in my opinion. I will have no problem doubling down on these positions if the tech sell-off continues.

A Software Update at GoPro (GPRO)

GoPro’s legacy business is involved in the sale of action cameras for adrenaline junkies and travelers. Its CEO originally destroyed the share price by overpaying himself in the early days after IPO (see below). Investors were also extremely worried about the rise of the smartphone and thought that GPROs action camera would become redundant as smartphone usage rose. This has not happened, and GoPro’s legacy action camera still dominates this niche today. It is now going through a huge transition to software, on top of the sale of its camera.

Its legacy business has pricing power, as customers are happy to pay more for the high-quality brand, but this side of the business has lower margins. Also, due to the durability of its cameras GPRO was unlikely to have repeat sales in any clear pattern. Recently the company has transformed, generating new streams of revenue through its cloud storage and video editing tools which have been added to its existing business. This, much like Airtel Africa, has given the business a funnel. GPRO can sell its cameras to customers and then receive recurring revenue through its cloud storage and video editing tools which are subscription-based, giving the company assured and constant cash flows at a higher margin.

The company has a 10% free cash flow yield and is priced at 5.6x EV/EBTIDA. The increase in subscriptions will help the business continue to expand margins and is seems to be an interesting opportunity with the ‘great reopening’ as people begin traveling and attending events again. This is an interesting opportunity and it is definitely a company close on my radar.

GoPro’s Subscriptions are on an exponential growth trend, Source: GoPro Investor Relations

Crocs (CROX) moving online

I found several interesting options with the likes of Buckle (BKE) and Dick’s Sporting Goods (DKS), but for the latter, I feel it is hard to find conviction with its large retail footprint as we move to online purchases. If the company were to sell down property to invest in its online business I would be very interested, as the company has over 2mn views on its website per day. Another issue with DKS is that a large part of sales comes from the resale of popular brands like Adidas, meaning they are at risk of a margin squeeze as inflation rises. This reason has recently made me uneasy regarding my current holding ASOS Plc (ASC). In addition to this, ASOS’s lack of free cash flow seems to be dragging on performance since I opened the position in December, as these more speculative growth stocks with a lack of cash will struggle in an environment of high inflation and tightening liquidity. For this reason, I have found a better opportunity in CROX as a clothing retailer for the portfolio.

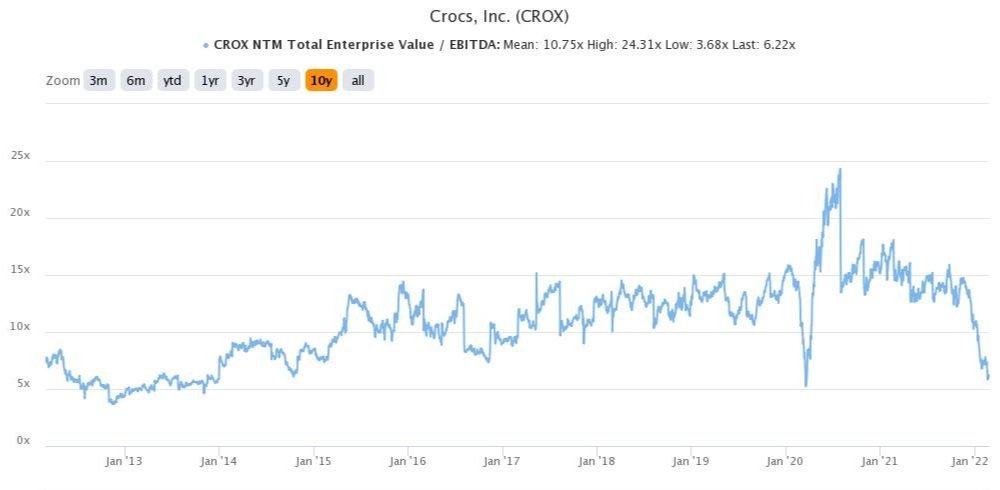

Croc’s has more favorable revenue growth (17% annualised into 2026) and a better free cash flow margin than ASC. It also has a far superior EBITDA margin at 31% (versus 7% for ASC) through its patented products, giving it better pricing power in higher inflation. Its huge shift to online and direct-to-consumer (DTC) sales should help continually strengthen these margins. CROX’s share price has been on a major run since the COVID Crash rising over 1000%, but it has now fallen back 50% and is at a very attractive valuation for the growth expected. Croc’s acquired Hey Dude during 2021 for $2.5bn, a price exceeding what investors saw as fair value, which was the primary reason for the huge sell-off. However, at current valuations, investors are getting this acquisition for free. Croc’s is also making huge strides in penetrating Asian markets for further growth and with over $1bn in stock repurchases during 2021, the company clearly sees continued growth and a stable financial position. I am adding a 2.3% position in the company.

Croc’s is as cheap as during the March 2020 crash, Source: TIKR Terminal

Diversified Growth Potential with PayPal (PYPL)

PayPal is a household name with over 425m active accounts across its business. It owns a number of payment processing apps including Venmo (send and receive money and purchase crypto) as well as Braintree (e-commerce payment solutions). With the huge market of customers across its family of apps the company has the optionality to cross-sell products as it continues to innovate into buy-now-pay-later (BNPL), cryptocurrencies, and stock investments as it expands its digital wallet. The number of crypto wallets currently stands at around 200m, roughly the same as the number of internet users in 2000. If I can find companies (such as Overstock and PayPal) who are exploiting this space while their legacy businesses produce cash flow, I will snap up such opportunities.

PayPal’s share price has been harshly affected by the recent tech sell-off, as well as weakened guidance by management due to supply chains, inflation, and weakening e-commence sales. I believe over the longer term these issues will be ironed out, and with the explosive growth of Fintech, PayPal has plenty of growth left in the tank. The company makes it money by charging a commission on goods sold through its apps. Therefore, by default, if inflation causes the price of goods to rise PayPal should benefit in some way.

PYPLs past and predicted revenue and margin growth is outstanding and its free cash flow, now standing at 5.2%, is almost unheard of for a high-growth tech company. The company also have an equity stake in Mercado Libre (think - Amazon of Latin America) which has more than doubled in value since they purchased the stake. With free cash flow growth from $5.4bn to $14bn by 2026, PYPL has huge optionality to use this cash to both expand current operations, make strategic acquisitions, and take stakes in other businesses. PayPal’s management has proved to be adept at doing so, with Joel Greenblatt’s measure of efficiency – Return on Capital – being 13% for PYPL. I am adding 2.3% to PayPal and if prices continue to drop, I will not be afraid to add to any of the aforementioned positions.

PYPL is as cheap as it has ever been, Source: TIKR

Actions:

· Adding 2.3% of capital to Crocs Inc (CROX) at

· Adding 2.3% of capital to PayPal (PYPL) at

· Adding 2.9% of capital to Meta Platforms (FB) at

· Adding 2.6% of capital to Digital Turbine (APPS) at

· Selling 100% of ASOS Plc (ASC) at £18.91, booking a 15% loss (£24.22)

Portfolio Return YTD: 3.9% vs S&P500 Return: -8.4%

Total Return since Inception (20/09/2021): 10% vs S&P500: 0.9%

Summary

The Russia-Ukraine crisis is continuing to escalate with discussion on whether Russian banks should be cut off from the SWIFT global payment system. There is likely to be continued volatility over the next few weeks (especially in energy markets) so I will remain patient and add to positions should a sell-off continue. My higher weighting to US dollar-denominated assets has helped add further performance gains. For UK-focused investors, purchasing TIP5 or converting cash to US Dollars until the turmoil passes may be a good idea.

Let me know your thoughts by emailing me at: thesparknewsletter@gmail.com

Until next time,

Peter

Disclaimer

This communication is for informational and educational purposes only and should not be taken nor used as investment advice, as a personal recommendation, or solicitation to buy or sell any financial instrument. This material has been prepared without considering any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or structured product are not, and should not be taken as, a reliable indicator of future performance. I assume no liability as to the accuracy or completeness of the content of this publication.